In August 2018, a group of Ethereum developers and entrepreneurs gathered in a Telegram chat and coined a term that would reshape how millions think about money: "decentralised finance," or DeFi. [4] Fast forward to 2026, and this concept has evolved from experimental protocols into a multi-billion-pound ecosystem that challenges centuries-old assumptions about how financial services should operate. Understanding what is DeFi has become essential for financial professionals, compliance officers, and serious investors navigating the intersection of blockchain technology and traditional finance,particularly in the UK, where regulatory frameworks continue to develop around these innovations. Explore more in our DeFi section.

Understanding What is DeFi: The Foundation

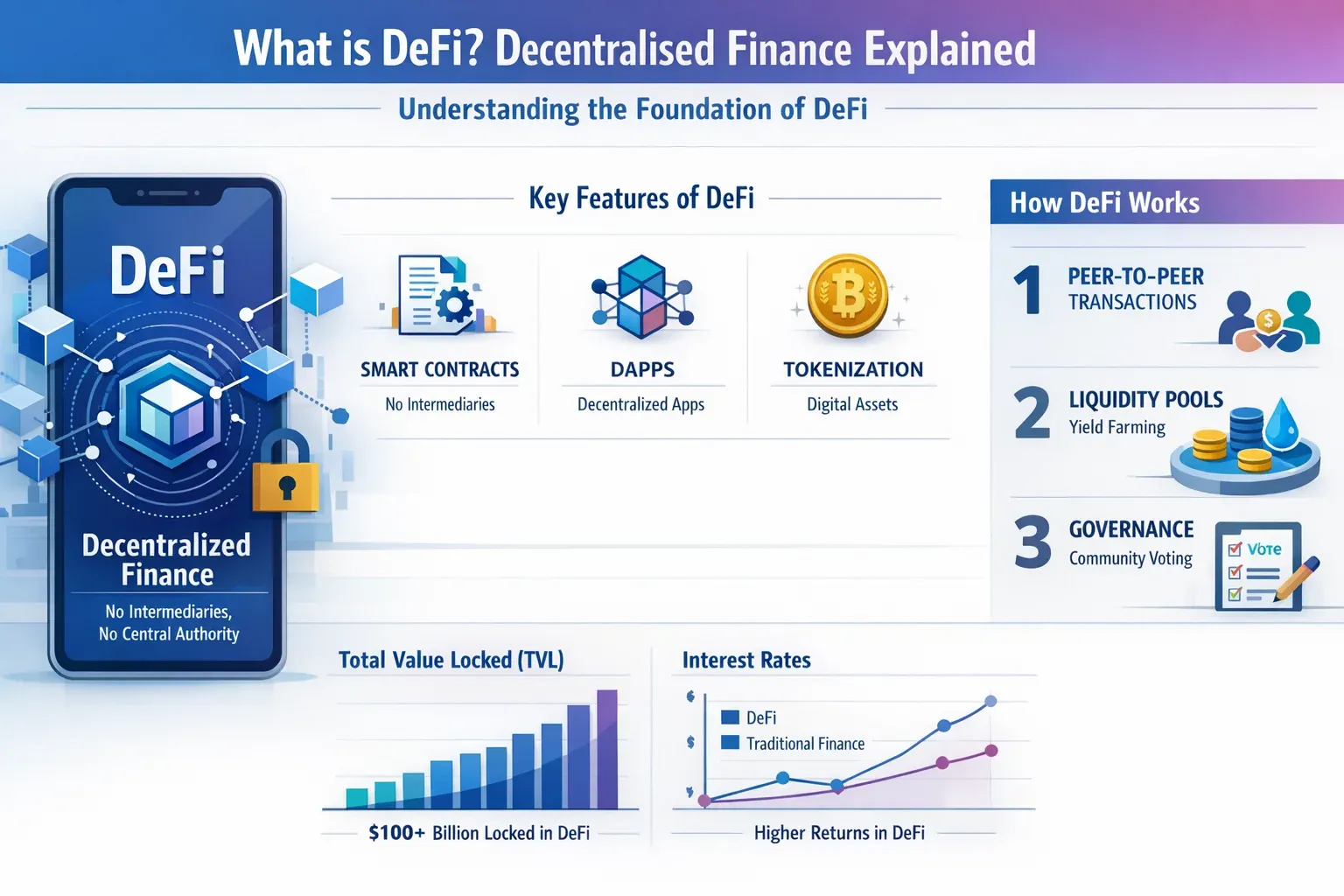

Decentralised finance represents a fundamental reimagining of financial infrastructure. Rather than relying on banks, exchanges, insurance companies, or other intermediaries to facilitate transactions and hold assets, DeFi operates through smart contracts,self-executing code deployed on blockchain networks, predominantly Ethereum. [1] [3]

The architectural difference is profound. Traditional finance operates through layers of intermediaries, each adding costs, delays, and points of potential failure. When you deposit funds in a bank, transfer money internationally, or trade securities, multiple institutions verify, process, and settle your transaction. Each intermediary maintains its own ledger, requiring reconciliation and introducing settlement risk.

DeFi protocols eliminate these intermediaries entirely. Smart contracts automatically execute financial functions when predetermined conditions are met, with all activity recorded on a public blockchain that serves as a single source of truth. [3] This shift from institution-based trust to code-based trust fundamentally changes the economics, accessibility, and risk profile of financial services.

The Core Principles of Decentralised Finance

Several defining characteristics distinguish DeFi from both traditional finance and centralised crypto platforms:

Permissionless Access: DeFi protocols are open to anyone with an internet connection and a compatible crypto wallet. [1] [2] There are no account applications, credit checks, minimum balance requirements, or geographic restrictions. A user in Manchester faces the same access conditions as someone in Mumbai or Miami.

Non-Custodial Architecture: Users maintain direct control of their assets through private keys rather than depositing funds with an intermediary. [1] This eliminates custodial risk,the possibility that a platform might be hacked, mismanage funds, or restrict withdrawals,but introduces self-custody responsibilities.

Transparency and Verifiability: All transactions, smart contract code, and protocol states are recorded on public blockchains. [3] [1] Anyone can verify the full transaction history, audit smart contract logic, and monitor protocol health in real-time,a level of transparency that private corporations rarely provide.

Composability: DeFi protocols function as "money legos," with standardised interfaces allowing them to interact seamlessly. [1] A user might deposit collateral in one protocol, borrow against it in a second, trade the borrowed assets on a third, and stake the proceeds in a fourth,all within minutes and often through a single interface.

Algorithmic Rate Determination: Rather than setting interest rates through committee decisions or opaque processes, DeFi protocols typically use algorithms that adjust rates based on supply and demand. [1] These rates often update every 15 seconds and can significantly exceed traditional banking rates, though they also carry different risk profiles. [3]

What is DeFi Used For? Core Applications and Use Cases

The DeFi ecosystem has developed sophisticated alternatives to nearly every traditional financial service. Understanding these applications helps clarify both the potential and limitations of decentralised finance.

Decentralised Exchanges (DEXs)

Decentralised exchanges enable peer-to-peer cryptocurrency trading without centralised order books or custodians. [1] Platforms like Uniswap and Curve use liquidity pools,smart contracts holding reserves of token pairs,to facilitate instant swaps at algorithmically determined prices.

When a user wants to exchange ETH for USDC, they interact directly with a liquidity pool smart contract rather than matching with another trader through a centralised exchange. The exchange rate adjusts based on the ratio of assets in the pool, with liquidity providers earning a portion of trading fees as compensation for supplying capital.

This model eliminates the need to deposit funds with an exchange, trust a centralised order matching system, or undergo identity verification. However, it introduces considerations around slippage (price impact of large trades), impermanent loss (opportunity cost for liquidity providers), and smart contract risk. Learn more with our tax loss harvesting calculator.

Lending and Borrowing Protocols

Protocols such as Aave and Compound create decentralised money markets where users can supply assets to earn interest or borrow against overcollateralised positions. [1] The mechanics differ substantially from traditional lending:

Supply Side: Users deposit cryptocurrency into lending pools, receiving interest that accrues continuously based on borrowing demand. Unlike traditional savings accounts with fixed rates set monthly or quarterly, DeFi lending rates adjust algorithmically,sometimes every 15 seconds,based on utilisation of the pool. [3]

Borrow Side: Borrowers must overcollateralise their positions, typically depositing £150-200 worth of assets to borrow £100. This eliminates credit risk and the need for credit checks, identity verification, or underwriting processes. [1] Liquidation occurs automatically through smart contracts if collateral value falls below required thresholds.

From a UK professional perspective, these protocols raise important questions about regulatory classification, tax treatment of earned interest, and whether activities constitute regulated financial services under FCA frameworks.

Yield Farming and Liquidity Mining

Yield farming involves depositing tokens into DeFi protocols to earn returns from multiple sources: trading fees, interest, and often governance tokens issued as incentives. [1] Aggregator services like Yearn Finance automate this process, moving capital between protocols to optimise returns.

The practice emerged as protocols sought to bootstrap liquidity and distribute governance tokens to users. While potentially lucrative, yield farming introduces complex risk considerations:

- Smart contract risk across multiple interconnected protocols

- Impermanent loss from providing liquidity to trading pairs

- Token price volatility affecting reward values

- Tax complexity from frequent transactions and multiple income sources

For UK taxpayers, HMRC guidance on DeFi taxation remains an evolving area. Professional advisors must help clients understand reporting obligations, whether activities constitute trading or investment, and how to value rewards received in governance tokens.

Synthetic Assets and Derivatives

DeFi enables creation of tokenised derivatives representing exposure to cryptocurrencies, commodities, equities, currencies, or indices,all without owning the underlying assets. [1] Protocols like Synthetix allow users to mint synthetic assets backed by collateral, creating on-chain exposure to traditional financial instruments.

These synthetic assets raise significant regulatory questions in the UK context. The FCA's financial promotion rules, which came into force in October 2023, impose strict requirements on marketing crypto assets. Synthetic assets representing securities may fall under existing securities regulation, whilst those tracking commodities or currencies face different regulatory treatment.

What is DeFi's Risk Profile? Understanding the Trade-offs

DeFi proponents often emphasise benefits like accessibility, transparency, and disintermediation. Professional advisors and serious investors must equally understand the distinct risks that accompany these advantages.

Smart Contract Vulnerabilities

Unlike traditional financial systems where human intermediaries can reverse erroneous transactions or freeze suspicious activity, DeFi smart contracts execute code exactly as written. [1] Bugs, logical errors, or unforeseen interactions can result in permanent loss of funds.

High-profile incidents illustrate this risk:

- The DAO hack (2016) exploited a smart contract vulnerability to drain approximately £50 million in ETH

- Numerous flash loan attacks have exploited protocol logic to extract millions

- Bridge hacks have resulted in some of the largest crypto thefts in history

Whilst smart contract auditing has become standard practice, audits provide no guarantee of security. Professional advisors should help clients understand that code is law in DeFi,there is no customer service department, no deposit insurance, and limited legal recourse when smart contracts behave as programmed but contrary to user expectations.

Self-Custody Responsibilities

DeFi's non-custodial architecture eliminates the risk that a platform might be hacked, freeze accounts, or misappropriate funds. However, it shifts security responsibility entirely to users. [1]

Private key management becomes critical. Lost private keys mean permanently inaccessible funds,no password reset process exists. Compromised keys allow irreversible theft. For institutional investors or high-net-worth individuals, this necessitates robust key management solutions, potentially including multi-signature wallets, hardware security modules, or qualified custodians.

The contrast with traditional finance is instructive. In centralised systems, users face custodial risk,the platform might be hacked or mismanage funds,but benefit from customer support, account recovery, and often regulatory protections. In DeFi, users eliminate custodial risk but assume full security responsibility.

Regulatory and Compliance Considerations

Perhaps the most significant challenge for UK-based users involves regulatory uncertainty and compliance obligations. Unlike traditional financial institutions that handle Know Your Customer (KYC) and Anti-Money Laundering (AML) functions on behalf of users, DeFi protocols operate permissionlessly. [1]

This creates several professional considerations:

Regulatory Classification: Are DeFi lending protocols offering regulated deposit-taking services? Do governance token holders operate collective investment schemes? The FCA continues developing its approach to these questions.

Tax Obligations: HMRC expects taxpayers to report crypto transactions, including DeFi activities. This requires maintaining detailed records of deposits, withdrawals, swaps, rewards earned, and fair market values,often across multiple protocols and hundreds of transactions.

AML Responsibilities: Whilst DeFi protocols don't implement KYC, UK users remain subject to anti-money laundering laws. Professional advisors should guide clients toward wallet screening tools and transaction monitoring to demonstrate proactive compliance.

Financial Promotion Rules: The FCA's crypto financial promotion rules, effective from October 2023, impose strict requirements on communicating about crypto assets. Advisors must ensure their DeFi-related communications include appropriate risk warnings, balanced information, and comply with categorisation requirements.

Liquidity and Market Risks

DeFi markets can experience extreme volatility and liquidity constraints, particularly during market stress. Unlike traditional markets with circuit breakers, trading halts, or central bank interventions, DeFi protocols continue operating through all market conditions.

This created significant challenges during events like:

- The March 2020 crypto market crash, when network congestion prevented timely liquidations

- May 2022's Terra/Luna collapse, which cascaded through interconnected DeFi protocols

- Various "bank run" scenarios on algorithmic stablecoins

Professional investors must understand that DeFi's 24/7 operation, whilst convenient, also means continuous exposure to market movements, potential liquidations outside traditional trading hours, and limited ability to pause or reverse transactions during extraordinary events.

Professional Standards and the Path Forward

For financial professionals considering DeFi,whether advising clients, managing institutional portfolios, or developing compliance frameworks,the technology demands a rigorous, evidence-based approach.

The Case for Professional Certification

The complexity of DeFi, combined with evolving UK regulation, creates clear need for professional standards. Just as traditional financial advisors pursue qualifications like the CFA or Chartered Financial Planner designation, crypto advisory professionals benefit from assessment-led certification that demonstrates competence across technical, regulatory, and ethical dimensions.

TrustCrypto Institute's approach mirrors the rigour of established financial professional bodies. Rather than promoting specific protocols or investment strategies, our frameworks focus on:

- Technical competence: Understanding blockchain architecture, smart contract mechanics, and protocol-specific risks

- Regulatory knowledge: Navigating FCA guidance, HMRC tax treatment, and UK-specific compliance obligations

- Ethical conduct: Transparent disclosures, appropriate risk warnings, and client-first advisory principles

- Continuing education: Maintaining current knowledge as protocols evolve and regulations develop

This standards-first approach serves both professionals seeking credibility and investors demanding accountability from advisors.

Practical Guidance for Serious Investors

For UK-based investors exploring DeFi, several principles support responsible participation:

Start Small and Learn Progressively: Begin with modest amounts on established protocols whilst developing technical understanding. The learning curve is substantial,smart contract interactions, gas fees, wallet security, and tax implications all require familiarity.

Prioritise Security: Invest in hardware wallets for significant holdings, use separate wallets for experimental protocols, verify contract addresses carefully, and never share private keys or seed phrases.

Maintain Detailed Records: HMRC expects comprehensive transaction records. Use portfolio tracking tools that integrate with DeFi protocols, document all deposits, withdrawals, swaps, and rewards, and retain evidence of fair market values.

Understand Tax Implications: DeFi activities typically trigger taxable events. Supplying liquidity, earning yield, swapping tokens, and receiving governance tokens each have tax consequences. Consult with crypto-competent tax advisors before executing complex strategies.

Seek Qualified Advice: The intersection of DeFi technology, UK regulation, and personal financial circumstances creates complexity that benefits from professional guidance. Look for advisors with verified credentials, transparent fee structures, and demonstrated technical competence,not influencers promoting specific protocols.

The Regulatory Outlook in the UK

The UK government and FCA continue developing their approach to crypto regulation, with DeFi presenting particular challenges. Unlike centralised platforms with identifiable operators, DeFi protocols often lack clear regulatory touchpoints.

Several developments merit attention:

The Financial Services and Markets Act 2023 grants HM Treasury power to regulate crypto assets, including stablecoins used in payments. This regulatory framework will likely expand to address DeFi activities.

The FCA's financial promotion rules already apply to DeFi-related communications, requiring authorised firms or appropriately approved communications when promoting crypto assets to UK consumers.

Tax guidance continues evolving, with HMRC publishing updated crypto tax manuals addressing DeFi-specific scenarios. Professional advisors must stay current with these developments to provide accurate guidance.

Looking forward, the UK appears to favour a principles-based regulatory approach that balances innovation with consumer protection,consistent with the jurisdiction's broader financial services philosophy. Professional standards bodies like TrustCrypto Institute play a crucial role in this ecosystem, establishing baseline competencies and ethical frameworks that complement formal regulation.

Conclusion: Substance Over Speculation

Understanding what is DeFi requires looking beyond both uncritical enthusiasm and reflexive dismissal. Decentralised finance represents genuine innovation in financial infrastructure,permissionless access, transparent operations, and disintermediated services offer meaningful advantages for certain use cases and user profiles.

Equally, DeFi introduces distinct risks: smart contract vulnerabilities, self-custody responsibilities, regulatory uncertainty, and complex tax obligations. These aren't hypothetical concerns but practical challenges that have resulted in billions in losses and significant compliance complications.

For UK-based financial professionals and serious investors, the path forward emphasises evidence-based assessment over speculation, professional standards over hype, and long-term perspective over short-term trends. DeFi technology will continue evolving, regulations will develop further clarity, and professional frameworks will mature.

Those who approach DeFi with appropriate rigour,investing in education, prioritising security, maintaining compliance, and seeking qualified guidance,position themselves to evaluate opportunities and risks with the seriousness they deserve. Those who chase yields without understanding mechanisms, ignore regulatory obligations, or follow influencer recommendations rather than conducting proper due diligence expose themselves to preventable losses.

The baseline for crypto knowledge and professional conduct continues rising. Whether you're an aspiring crypto advisor seeking credible qualifications, a compliance professional navigating regulatory complexity, or an investor demanding accountability from advisors, professional standards matter. The difference between competent DeFi participation and costly mistakes often comes down to structured knowledge, rigorous assessment, and commitment to ethical practice.

TrustCrypto Institute exists to raise that baseline,providing clear frameworks, assessment-led certification, and evidence-based education for professionals who value substance over speculation. Because in DeFi, as in all finance, credibility and competence aren't optional extras. They're the foundation of sustainable practice.

Take the Next Step

Ready to advance your crypto expertise? Explore our TCCS certification to enhance your professional credentials.

References

- [1] Decentralized Finance - https://www.trmlabs.com/glossary/decentralized-finance

- [2] Defi - https://www.masterclass.com/articles/defi

- [3] What Is Defi - https://www.coinbase.com/learn/crypto-basics/what-is-defi

- [4] Decentralized Finance Defined - https://www.fidelity.com/learning-center/trading-investing/crypto/decentralized-finance-defined