As interest in digital assets grows, many investors are asking about crypto pension UK options and whether they can include cryptocurrencies in their retirement portfolios. Current HMRC regulations place significant restrictions on holding crypto assets within UK pension schemes, including SIPPs. This guide explains the key rules and considerations for anyone looking to combine cryptocurrency investments with their pension strategy. Explore more in our Finance section.

The promise of tax-efficient retirement savings meets the volatility of digital assets in one of the most frequently asked questions facing UK investors in 2026: can you actually hold cryptocurrency within a Self-Invested Personal Pension (SIPP)? While institutional pension funds have begun tentative allocations to Bitcoin, the rules governing individual pension schemes tell a markedly different story,one grounded in HMRC guidance that fundamentally challenges the tax advantages investors expect from pension wrappers.

Understanding whether you can hold crypto in a UK pension requires navigating the intersection of pension legislation, cryptoasset taxation, and evolving regulatory frameworks. The answer is more nuanced than a simple yes or no, with significant implications for tax relief, compliance, and long-term retirement planning.

Understanding UK SIPP Rules and Permitted Investments

Self-Invested Personal Pensions represent one of the most flexible pension vehicles available to UK investors, traditionally offering broad investment powers across equities, bonds, commercial property, and alternative assets. The appeal lies in the combination of investment control and substantial tax advantages,including income tax relief on contributions, tax-free growth within the wrapper, and a 25% tax-free lump sum at retirement.

However, permitted investments within SIPPs are governed by strict HMRC rules designed to prevent abuse of pension tax reliefs. The Financial Services and Markets Act 2000 and subsequent pension legislation establish clear boundaries around what constitutes an acceptable pension investment.

Traditional SIPP Investment Universe

Standard SIPP platforms typically permit:

- Listed equities and bonds on recognised exchanges

- Collective investment schemes (unit trusts, OEICs, investment trusts)

- Commercial property (subject to specific rules)

- Cash deposits

- Exchange-traded funds and exchange-traded commodities

The common thread connecting these assets is regulatory oversight, established valuation methodologies, and recognition within existing tax frameworks.

The Cryptoasset Challenge

Cryptocurrency introduces complications on multiple fronts. Unlike traditional securities, cryptoassets exist outside conventional financial infrastructure, lack standardised custody arrangements, and,critically for pension purposes,are not treated by HMRC as equivalent to money or fiat currency [1].

This classification creates a fundamental tension with pension tax rules, which were designed around traditional asset classes with clear regulatory status and established market infrastructure.

Can You Hold Crypto in a UK Pension? The Tax Relief Problem

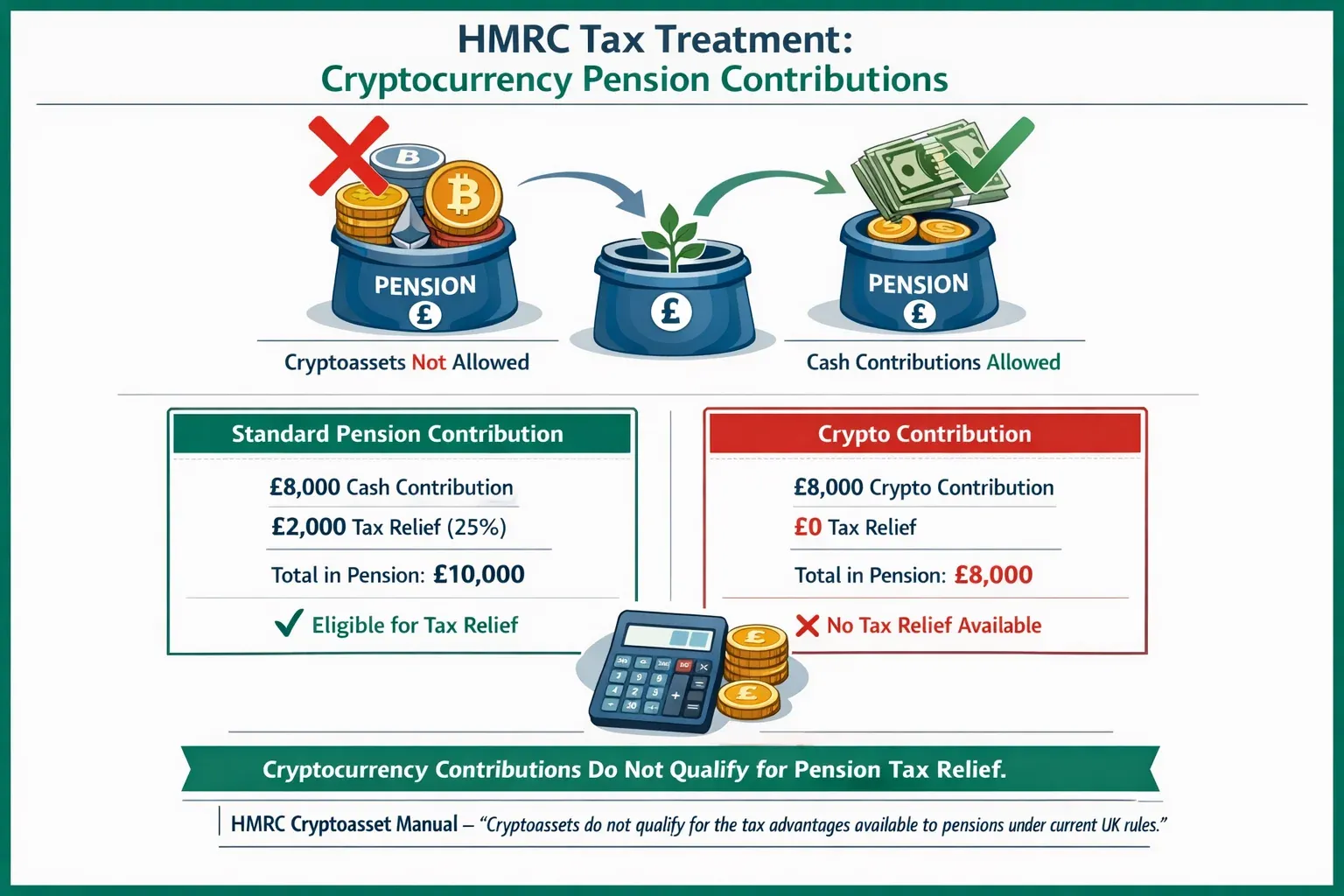

The most significant barrier to holding cryptocurrency in a UK pension centres on tax relief eligibility. According to HMRC's Cryptoasset Manual (CRYPTO), updated in May 2025, cryptoassets contributed to pension funds are not treated as tax-relievable contributions [1].

This guidance effectively removes the primary financial incentive for holding crypto within a pension wrapper.

How Pension Tax Relief Normally Works

Under standard pension contribution rules:

- An individual contributes £10,000 to their SIPP

- HMRC automatically adds 25% basic rate tax relief (£2,500)

- Higher-rate taxpayers claim additional relief through self-assessment

- The pension receives £12,500 for a £10,000 net contribution (for basic rate taxpayers)

This tax advantage represents the cornerstone of pension investing, turning retirement savings into one of the most tax-efficient investment vehicles available.

Why Crypto Contributions Don't Qualify

HMRC's position stems from the classification of cryptoassets as property rather than currency [1]. Pension tax relief provisions were designed for monetary contributions,pounds sterling entering a pension scheme. When an individual attempts to contribute Bitcoin or Ethereum directly, HMRC views this as a property transfer rather than a monetary contribution.

The practical implications are severe:

- ❌ No automatic 25% tax relief on crypto contributions

- ❌ No higher-rate tax relief claims

- ❌ Potential tax charges on the disposal of crypto before pension contribution

- ❌ Elimination of the primary pension tax advantage

> "HMRC does not treat any currently available cryptoassets as equivalent to money or fiat currency, which affects how pension tax rules apply to crypto holdings." , HMRC Cryptoasset Manual [1]

This creates a scenario where holding crypto in a pension offers no tax advantage over holding it in a standard taxable account,and potentially creates additional complexity and cost.

SIPP Provider Policies on Cryptocurrency Holdings

Beyond HMRC's tax treatment, individual SIPP providers maintain their own investment restrictions based on regulatory risk, custody capabilities, and compliance frameworks. As of 2026, the landscape remains fragmented and restrictive.

Mainstream Provider Restrictions

The majority of established SIPP providers,including major platforms operated by insurance companies, wealth managers, and investment platforms,do not permit direct cryptocurrency holdings. Their restrictions stem from:

Regulatory uncertainty: The evolving UK cryptoasset regulatory framework creates compliance challenges for pension administrators [2] [3].

Custody concerns: Traditional pension custody arrangements are designed for securities held through CREST or similar systems, not blockchain-based assets requiring private key management.

Valuation difficulties: HMRC requires pension assets to be valued annually for reporting purposes. Cryptocurrency volatility and 24/7 trading create practical challenges for standardised valuation.

FCA authorisation requirements: The new cryptoasset regime requires firms facilitating crypto activities to hold appropriate FCA permissions, which many traditional pension providers have not sought [5].

Specialist SIPP Platforms

A small number of specialist SIPP providers have emerged offering limited cryptocurrency exposure, typically through:

- Exchange-traded products (ETPs) tracking cryptocurrency prices

- Cryptocurrency-focused investment trusts (where available)

- Indirect exposure through equities of crypto-related businesses

These structures attempt to provide crypto exposure while remaining within traditional securities frameworks that SIPP administrators can accommodate. However, they introduce additional layers of fees and may not track underlying cryptocurrency performance precisely.

The Direct Holding Question

True direct holding of cryptocurrency,where the SIPP itself holds private keys to Bitcoin or Ethereum,remains exceptionally rare among UK SIPP providers. The combination of regulatory uncertainty, custody complexity, and HMRC's tax treatment creates substantial barriers that most administrators consider prohibitive.

The Institutional Exception: Pension Funds vs. Individual SIPPs

An important distinction exists between institutional defined benefit pension schemes and individual SIPPs. This became evident in October 2024 when a UK defined benefit pension fund made history by allocating 3% of its portfolio to Bitcoin [7].

Why Institutional Funds Have Different Options

Defined benefit pension schemes operate under different regulatory frameworks than individual SIPPs:

Professional governance: Institutional schemes have dedicated trustees and investment committees with fiduciary responsibilities.

Sophisticated custody: Large pension funds can negotiate bespoke custody arrangements with specialist providers.

Different tax treatment: Institutional pension fund contributions and investment structures operate under separate tax provisions from individual pension tax relief.

Regulatory oversight: The Pensions Regulator provides direct oversight of defined benefit schemes, creating a different compliance environment.

The 2024 Bitcoin allocation by a UK pension fund represents an institutional investment decision rather than evidence that individual SIPP holders can replicate the same approach [7]. The fund likely used specialist custody services, institutional-grade trading infrastructure, and obtained specific trustee approval,none of which translate to the individual SIPP environment.

What This Means for Individual Investors

The institutional precedent demonstrates growing acceptance of cryptocurrency as an asset class within professional investment frameworks. However, individual SIPP investors cannot assume the same access or treatment. The regulatory, custody, and tax frameworks governing individual pensions remain distinct and more restrictive.

The Regulatory Landscape: What's Changing in 2026-2027

The UK cryptoasset regulatory environment is undergoing significant transformation, with implications for pension-related questions. The comprehensive UK cryptoasset regulatory framework comes into force on 25 October 2027 [2] [3], establishing a new regulatory perimeter for digital assets.

Key Regulatory Developments

Financial Services and Markets Act 2000 (Cryptoassets) Regulations 2026: Published in early 2026, these regulations establish the legal framework for bringing cryptoassets within financial services regulation [4].

FCA cryptoasset regime: The Financial Conduct Authority's new regulatory approach covers cryptoasset activities including trading, custody, and advice [5].

Ongoing HMRC guidance: The Cryptoasset Manual continues to evolve, though current provisions maintain the position that crypto contributions do not qualify for pension tax relief [1].

What Remains Unclear for Pensions

Despite regulatory progress, specific guidance on cryptocurrency within individual pension schemes remains limited. The 2027 framework focuses primarily on:

- Consumer protection for cryptoasset activities

- Market integrity and financial crime prevention

- Prudential requirements for cryptoasset firms

- Financial promotion standards

Pension-specific provisions have not been prominently addressed in current regulatory consultations, suggesting this area may require separate policy development [2] [3].

Potential Future Developments

Several scenarios could alter the pension-crypto landscape:

HMRC policy revision: A future change to cryptoasset classification could enable tax relief on crypto pension contributions, though no indication of such change exists in current guidance.

Regulated custody solutions: As the FCA cryptoasset regime matures, regulated custody providers may emerge with capabilities that satisfy pension administrator requirements.

Pension legislation updates: Specific amendments to pension rules could explicitly address cryptoasset holdings, either permitting them under certain conditions or formally prohibiting them.

Until such developments materialise, the current restrictive environment is likely to persist.

Practical Alternatives for Crypto Exposure in Retirement Planning

For UK investors seeking cryptocurrency exposure within a tax-efficient structure, several alternatives to direct SIPP holdings merit consideration,each with distinct trade-offs.

1. Crypto-Related Equities Within SIPPs

Investing in publicly listed companies with significant cryptocurrency exposure provides indirect participation while remaining within traditional SIPP investment universes:

- Cryptocurrency exchanges (Coinbase, etc.)

- Bitcoin mining companies

- Blockchain technology firms

- Payment processors with crypto capabilities

Advantages: Full pension tax relief, established custody, regulatory clarity Disadvantages: Company-specific risk, imperfect correlation with crypto prices, equity market exposure

2. Cryptocurrency ETPs and Investment Trusts

Exchange-traded products tracking cryptocurrency prices or investment trusts with crypto mandates offer more direct exposure:

- Bitcoin and Ethereum exchange-traded commodities

- Cryptocurrency-focused investment trusts (where available)

- Blockchain technology ETFs

Advantages: Closer price tracking, pension tax relief eligibility, professional management Disadvantages: Management fees, tracking error, limited product availability in UK

3. ISA Wrappers for Direct Crypto Holdings

While not pension-related, Innovative Finance ISAs (IFISAs) or standard Investment ISAs might accommodate certain crypto-related investments:

Advantages: Tax-free growth and withdrawals, greater flexibility than pensions Disadvantages: No tax relief on contributions, £20,000 annual limit, most providers don't offer direct crypto

4. Taxable Crypto Holdings with Tax Planning

Holding cryptocurrency outside tax wrappers while employing strategic tax planning:

- Utilising annual Capital Gains Tax allowance (£3,000 in 2026)

- Timing disposals across tax years

- Spouse transfers to maximise allowances

- Detailed record-keeping for HMRC reporting

Advantages: Direct ownership, full control, access to entire crypto universe Disadvantages: No tax relief, CGT on gains, income tax on certain crypto activities

5. Waiting for Regulatory Clarity

Given the evolving regulatory landscape and the October 2027 implementation of comprehensive cryptoasset regulation [2] [3], some investors may choose to defer pension-crypto integration until clearer frameworks emerge.

This approach prioritises regulatory certainty over immediate exposure, recognising that premature structuring could create tax complications or compliance issues.

Professional Standards and Crypto Pension Advice

The complexity surrounding cryptocurrency in UK pensions underscores the critical importance of qualified, competent professional advice. The intersection of pension legislation, cryptoasset taxation, and evolving regulation creates substantial scope for costly errors.

The Role of Qualified Advisors

Financial advisors addressing crypto-pension questions must demonstrate:

Pension expertise: Deep understanding of SIPP rules, pension tax relief, and retirement planning frameworks.

Cryptoasset knowledge: Technical comprehension of blockchain technology, cryptocurrency characteristics, and digital asset risks.

Regulatory awareness: Current knowledge of FCA cryptoasset regulation, HMRC tax treatment, and evolving policy landscape [1] [5].

Evidence-based methodology: Recommendations grounded in regulatory guidance rather than speculation or promotional material.

Assessment-Led Certification

The emergence of professional standards for crypto advisory through assessment-led certification helps investors identify advisors with verified competence. Rigorous assessment ensures advisors understand:

- HMRC's current position on cryptoasset pension contributions

- SIPP provider capabilities and restrictions

- Alternative structures for tax-efficient crypto exposure

- Risk disclosure requirements and consumer protection obligations

Standards matter when navigating uncharted territory. The crypto-pension intersection represents precisely the type of complex, evolving area where professional accountability and transparent credentials provide essential consumer protection.

Red Flags in Crypto Pension Advice

Investors should exercise caution when encountering:

- ❌ Guarantees of pension tax relief on crypto contributions (contradicts HMRC guidance)

- ❌ Promotion of unregulated SIPP structures or offshore arrangements

- ❌ Advice that ignores HMRC's Cryptoasset Manual provisions

- ❌ Pressure to act quickly before "regulatory windows close"

- ❌ Advisors without verifiable credentials or professional indemnity insurance

Substance over speculation applies particularly to pension planning, where mistakes can have decades-long consequences.

Risk Considerations and Long-Term Perspective

Beyond regulatory and tax questions, fundamental risk considerations apply to any contemplation of cryptocurrency within retirement portfolios.

Volatility and Retirement Security

Cryptocurrency markets exhibit extreme volatility relative to traditional pension assets. Bitcoin's historical price swings,including 80%+ drawdowns during bear markets,create substantial sequence-of-returns risk for retirees.

Pension funds serve a specific purpose: providing reliable income during retirement when earning capacity has ceased. The risk-return profile of cryptocurrency may be inappropriate for this objective, regardless of regulatory status.

Custody and Security Risks

Even if regulatory frameworks evolve to permit crypto in SIPPs, custody risk remains fundamental:

- Private key loss or theft

- Exchange hacks or insolvency

- Smart contract vulnerabilities

- Operational errors in pension administration

Traditional pension assets benefit from established custody frameworks, compensation schemes, and regulatory protections. Cryptocurrency custody introduces novel risks that pension savers must carefully evaluate.

Market Cycle Awareness

Professional crypto advisory employs cycle-aware strategy recognising that digital asset markets move through distinct phases. The institutional pension fund allocation in October 2024 occurred after a significant market correction, potentially representing strategic timing rather than all-weather positioning [7].

Retail investors considering crypto exposure,whether in pensions or elsewhere,benefit from long-term perspective and understanding of market cycles rather than reactive decision-making.

Conclusion: Navigating Crypto and UK Pensions in 2026

Can you hold crypto in a UK pension? The technical answer is that some specialist SIPP providers may offer limited indirect exposure, but the practical reality is far more restrictive than many investors anticipate. HMRC's clear position that cryptoassets contributed to pension funds do not qualify for tax relief eliminates the primary advantage of pension wrappers [1].

The distinction between institutional pension funds,which have begun modest Bitcoin allocations,and individual SIPPs remains critical [7]. Different regulatory frameworks, custody capabilities, and tax treatments mean individual investors cannot simply replicate institutional approaches.

As the comprehensive UK cryptoasset regulatory framework approaches implementation in October 2027 [2] [3], clarity may eventually emerge. Until then, investors face a landscape characterised by:

- Limited SIPP provider options for direct crypto holdings

- No pension tax relief on cryptoasset contributions

- Evolving but incomplete regulatory frameworks

- Alternative structures offering indirect exposure with trade-offs

Actionable Next Steps

For investors considering cryptocurrency within retirement planning:

- Verify current HMRC guidance on cryptoasset pension contributions before making any decisions

- Consult qualified professionals with verified credentials in both pension planning and cryptoassets

- Evaluate alternatives including crypto-related equities, ETPs, or taxable holdings with tax planning

- Consider timing given the October 2027 regulatory implementation that may clarify provisions

- Maintain perspective on cryptocurrency's role within overall retirement strategy and risk tolerance

The intersection of cryptocurrency and UK pensions represents an evolving area where professional standards, regulatory compliance, and evidence-based advice prove essential. Investors benefit from approaching these questions with the same rigour and long-term thinking that characterises sound retirement planning,prioritising substance over speculation and verified competence over promotional hype.

As regulatory frameworks mature and institutional adoption progresses, the landscape may shift. For now, understanding current rules, recognising limitations, and making informed decisions within existing frameworks represents the prudent path forward.

Related Resources

Explore these helpful tools and guides:

Take the Next Step

Ready to advance your crypto expertise? Explore our professional certification programmes to enhance your credentials.

References

- [1] United Kingdom - https://www.globallegalinsights.com/practice-areas/blockchain-cryptocurrency-laws-and-regulations/united-kingdom/

- [2] Uk Cryptoasset Regulation Action Points For 2026 2027 - https://www.sidley.com/en/insights/newsupdates/2026/01/uk-cryptoasset-regulation-action-points-for-2026-2027

- [3] Uk Makes Crypto Legislation - https://financialregulation.linklaters.com/post/102mgxj/uk-makes-crypto-legislation

- [4] Financial Services And Markets Act 2000 Cryptoassets Regulations 2026 Published - https://www.regulationtomorrow.com/eu/financial-services-and-markets-act-2000-cryptoassets-regulations-2026-published/

- [5] New Regime Cryptoasset Regulation - https://www.fca.org.uk/firms/new-regime-cryptoasset-regulation

- [6] Cryptoassets - https://www.gov.uk/government/collections/cryptoassets

- [7] Uk Pension Fund Bitcoin Allocation Reshaping Institutional Thinking - https://zodiamarkets.com/blog/uk-pension-fund-bitcoin-allocation-reshaping-institutional-thinking/

- [8] Crypto Regulation In The Uk - https://cms.law/en/gbr/publication/crypto-regulation-in-the-uk