Many UK crypto investors ask when do I pay tax on crypto UK. This guide covers everything you need to know about cryptocurrency taxation, updated for 2026. Explore more in our Policy section.

You've just sold some Bitcoin at a profit. Brilliant. But here's the question that should immediately follow: have you just triggered a tax liability? If you're asking "when do I pay tax on crypto UK?" after the fact, you're not alone,but you might already be behind the curve. The reality is that HMRC has clear, specific rules about cryptocurrency taxation, and ignorance isn't a defence that holds up well during an investigation.

At TrustCrypto Institute, we've seen countless professionals and investors stumble over UK crypto tax obligations,not because the rules are impossibly complex, but because they're often misunderstood or discovered too late. This isn't about scaremongering. it's about professional accountability and protecting yourself from entirely avoidable penalties.

This comprehensive guide will walk you through exactly when you need to pay tax on crypto in the UK, what triggers a taxable event, how HMRC expects you to report it, and the critical deadlines you cannot afford to miss. We're grounding everything in current HMRC guidance and UK tax law as it stands in 2026, with the evidence-based approach you'd expect from an independent standards body.

Understanding HMRC's Position on Cryptocurrency

HMRC doesn't consider cryptocurrency to be currency or money. Instead, the tax authority treats crypto assets as property for tax purposes [1]. This fundamental classification shapes every aspect of how crypto is taxed in the UK.

According to HMRC's Cryptoassets Manual (published and regularly updated since 2018), cryptoassets include Bitcoin, Ethereum, and other exchange tokens, utility tokens, security tokens, and stablecoins [2]. This broad definition means that virtually every digital asset you might hold falls under UK tax rules.

The classification as property rather than currency has significant implications. When you dispose of property, you potentially trigger Capital Gains Tax. When you receive property as payment for services, you face Income Tax. This dual-tax framework is where many people get confused about when do I pay tax on crypto UK obligations actually arise.

HMRC has been remarkably clear in its guidance: the tax treatment depends on the nature of your activities and the type of tokens involved. There's no blanket exemption for crypto, no special "digital asset" tax rate, and no grace period for small investors. The rules apply universally, whether you're holding £100 or £10 million in crypto assets.

The Legal Framework Behind Crypto Taxation

The UK's approach to crypto taxation rests on existing tax legislation rather than crypto-specific laws. The Taxation of Chargeable Gains Act 1992 governs Capital Gains Tax, while the Income Tax (Trading and Other Income) Act 2005 and Income Tax (Earnings and Pensions) Act 2003 cover income-related crypto taxation [3].

This means HMRC applies established tax principles to a new asset class. The authority has stated that it will look at each case individually, considering the specific facts and circumstances. However, certain patterns have emerged that provide clarity for most situations.

For professionals advising clients on crypto taxation,or investors managing their own compliance,understanding this legal foundation is essential. We're not dealing with experimental or untested regulation here. These are well-established tax principles applied to digital assets, backed by decades of case law around property disposal and income recognition.

When Do I Pay Tax on Crypto UK? The Taxable Events Explained

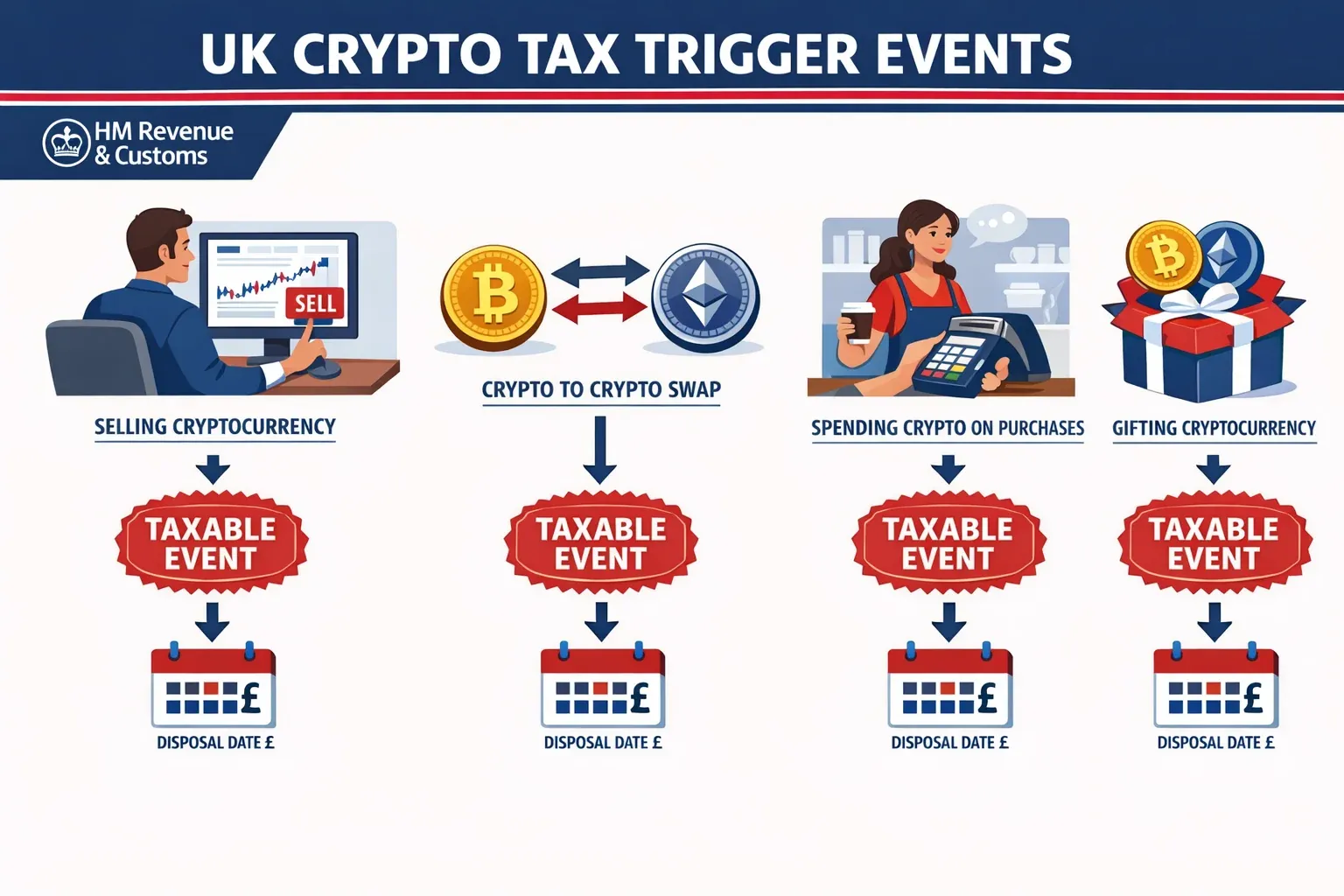

The critical question,when do I pay tax on crypto UK?,has a straightforward answer: you pay tax when you dispose of cryptocurrency or receive it as income. But "disposal" covers more scenarios than most people realise.

Taxable Crypto Disposals

HMRC defines disposal broadly. You've disposed of cryptocurrency when you:

Sell crypto for fiat currency (pounds, dollars, euros, etc.). This is the most obvious taxable event. If you sell Bitcoin for £10,000 and your original cost basis was £6,000, you've realised a £4,000 gain that may be subject to Capital Gains Tax.

Exchange one cryptocurrency for another. This catches many people off guard. Trading Bitcoin for Ethereum, swapping stablecoins for altcoins, or any crypto-to-crypto transaction is a disposal of the original asset. You must calculate the pound sterling value of both cryptocurrencies at the time of the exchange to determine your gain or loss [4]. Learn more with our tax loss harvesting calculator.

Use crypto to pay for goods or services. Spent Bitcoin on a car? Used Ethereum to pay for consulting services? That's a disposal. You need to calculate the difference between what you paid for the crypto originally and its value when you spent it.

Gift crypto to another person (unless it's to your spouse or civil partner). Gifts are treated as disposals at market value, potentially triggering a Capital Gains Tax liability even though you received no cash.

Exchange crypto for a different type of token (such as wrapped tokens or when tokens migrate to new contracts). Even technical exchanges can trigger tax events.

Trade crypto using derivatives or contracts for difference. These sophisticated trading activities create their own tax obligations.

What Isn't a Taxable Event

It's equally important to understand what doesn't trigger a tax liability:

- Buying crypto with fiat currency and holding it. Purchasing cryptocurrency creates your cost basis but doesn't trigger tax until you dispose of it.

- Transferring crypto between your own wallets. Moving Bitcoin from Coinbase to your hardware wallet isn't a disposal,you still own the asset.

- Donating crypto to a registered charity. Charitable donations of crypto are generally exempt from Capital Gains Tax [5].

- Transferring crypto to your spouse or civil partner. These transfers are treated as "no gain/no loss" transactions.

Understanding these distinctions is fundamental to answering when do I pay tax on crypto UK. The timing of your tax obligation is directly tied to the timing of these disposal events.

Capital Gains Tax vs Income Tax: Which Applies?

Not all crypto taxation is created equal. HMRC distinguishes between:

Capital Gains Tax treatment: This applies to most individual investors who buy and hold crypto as an investment. You calculate gains by subtracting your cost basis (what you paid, including fees) from your disposal proceeds (what you received). You can deduct allowable costs like transaction fees and, in 2026, you benefit from the annual Capital Gains Tax allowance (currently £3,000) [6].

Capital Gains Tax rates for 2026 are 10% (basic rate taxpayers) or 20% (higher and additional rate taxpayers) for most assets, though these rates are subject to change in each Budget.

Income Tax treatment: This applies when you receive crypto as income,through employment, mining, staking rewards (in most cases), airdrops received in exchange for services, or if HMRC considers your crypto activity to be trading rather than investing.

Income Tax rates are significantly higher, ranging from 20% to 45% depending on your total income, plus National Insurance contributions may apply [7].

The distinction matters enormously. A £10,000 crypto gain might result in £2,000 tax under Capital Gains Tax (at 20%) but could cost £4,500 under Income Tax (at 45% for additional rate taxpayers).

How HMRC Determines If You're Trading or Investing

One of the most consequential questions in crypto taxation is whether HMRC will view your activities as investing (Capital Gains Tax) or trading (Income Tax). This isn't a choice you make,it's a determination HMRC makes based on the facts.

The Badges of Trade

HMRC applies the traditional "badges of trade" test, developed through decades of tax case law, to crypto activities [8]. These include:

Frequency of transactions: Are you making dozens of trades per week or a few per year? High-frequency trading suggests a trade rather than investment.

Organisation and sophistication: Do you use trading bots, maintain detailed spreadsheets, employ technical analysis, or treat crypto activities like a business? These factors point toward trading.

Source of finance: Did you borrow money specifically to fund crypto purchases? Trading businesses often use leverage.

Holding period: Do you hold crypto for years or flip it within days? Long holding periods suggest investment. short periods suggest trading.

Reason for acquisition: Did you buy crypto to hold long-term or to profit from short-term price movements?

Method of acquisition: Did you acquire crypto in a way consistent with investment (regular purchases) or trading (buying specifically to resell)?

For most individuals holding crypto as part of a diversified portfolio, making occasional sales, and not operating in a business-like manner, Capital Gains Tax treatment applies. But if you're day-trading, using significant leverage, or treating crypto as your primary income source, HMRC may determine you're trading.

This determination affects not just tax rates but also what expenses you can deduct, how losses are treated, and your reporting obligations. If you're uncertain which category applies to you, this is precisely where professional advice from a qualified crypto advisor becomes invaluable.

Specific Crypto Activities and Their Tax Treatment

Let's examine common crypto activities and their specific tax implications under HMRC rules.

Mining Cryptocurrency

Cryptocurrency mining typically receives Income Tax treatment. HMRC views mining as a service you provide to the blockchain network in exchange for crypto rewards [9].

Hobby mining: If you mine crypto casually, the tokens you receive are taxable income at their pound sterling value when you receive them. You can deduct the direct costs of mining (electricity, equipment depreciation) from this income.

Mining as a trade: If you mine on a commercial scale, you're running a business. You'll pay Income Tax and potentially National Insurance on your profits. You can deduct business expenses, but you also have more complex reporting requirements.

When you later sell the crypto you mined, that's a separate Capital Gains Tax event. Your cost basis is the value you declared as income when you received the mining rewards.

Staking Rewards and Yield Farming

HMRC's position on staking has evolved, but the current guidance treats most staking rewards as income when received [10].

Proof-of-Stake validation rewards: If you stake Ethereum or other PoS tokens and receive rewards, these are typically taxable as income at their value when you receive them.

DeFi yield farming: Returns from liquidity provision, yield farming, or lending protocols are generally treated as income. The complexity here is significant,you may have multiple taxable events including providing liquidity (potential disposal), receiving governance tokens (income), and claiming rewards (income).

Locked staking: Even if rewards are locked or vested, HMRC may consider them taxable when you gain the right to them, not when you can access them. The specific facts matter here.

Airdrops and Forks

The tax treatment of airdrops depends on why you received them:

Airdrops for holding existing tokens: If you receive an airdrop simply for holding a particular cryptocurrency, HMRC generally treats this as a capital receipt that increases your cost basis rather than immediate income. However, when you dispose of the airdropped tokens, you'll pay Capital Gains Tax [11].

Airdrops for services: If you received tokens in exchange for promoting a project, providing services, or completing tasks, that's income taxable when received.

Hard forks: When a blockchain forks and you receive new tokens (like when Bitcoin Cash split from Bitcoin), HMRC's position is that you haven't received income. Instead, your original cost basis is split between the original and new tokens. You'll pay Capital Gains Tax when you dispose of either.

NFTs (Non-Fungible Tokens)

NFTs are treated as cryptoassets for tax purposes. Buying an NFT isn't taxable, but selling one, trading it, or using it commercially triggers tax:

Selling an NFT: Capital Gains Tax applies on the difference between your purchase price and sale price.

Creating and selling NFTs: If you're an artist or creator selling NFTs, HMRC may treat this as trading income subject to Income Tax, particularly if you're doing it regularly or commercially.

Using cryptocurrency to buy NFTs: This is a disposal of the crypto you spent, potentially triggering Capital Gains Tax on that crypto.

When Do I Pay Tax on Crypto UK? Understanding Tax Year Deadlines

Understanding when taxable events occur is only half the equation. You also need to know when do I pay tax on crypto UK in terms of actual deadlines for reporting and payment.

The UK Tax Year

The UK tax year runs from 6 April to 5 April the following year. Any crypto disposals you make during this period must be reported together. For the current 2026/27 tax year, this means 6 April 2026 to 5 April 2027.

This timing matters because your Capital Gains Tax allowance (£3,000 for 2026/27) applies per tax year. Strategic timing of disposals across tax years can significantly reduce your tax liability.

Registration Deadlines

If you need to complete a Self Assessment tax return (which you will if you have crypto gains above the annual allowance or crypto income to report), you must register with HMRC:

- By 5 October following the end of the tax year if you've never filed a Self Assessment before

- If you're already in Self Assessment, you don't need to re-register

For example, if you made taxable crypto disposals in the 2026/27 tax year (6 April 2026 to 5 April 2027), and you've never filed Self Assessment before, you must register by 5 October 2027.

Filing Deadlines

Once registered, you face two possible deadlines depending on how you file:

- 31 October following the end of the tax year for paper returns

- 31 January following the end of the tax year for online returns

In practice, almost everyone files online. For the 2026/27 tax year, your online Self Assessment return would be due by 31 January 2028.

Payment Deadlines

Tax payment follows the same deadline as online filing: 31 January following the end of the tax year.

For the 2026/27 tax year, you would need to pay any Capital Gains Tax or Income Tax owed by 31 January 2028.

If your tax bill exceeds £1,000, you may also need to make payments on account,advance payments toward the next year's tax bill,due on 31 January and 31 July [12].

Real-World Timeline Example

Let's make this concrete:

15 August 2026: You sell Bitcoin for a £25,000 gain. This occurs in the 2026/27 tax year.

5 October 2027: Deadline to register for Self Assessment (if you're not already registered).

31 January 2028: Deadline to file your 2026/27 Self Assessment return online and pay any tax due.

Missing these deadlines triggers penalties. Late filing penalties start at £100 and increase the longer you delay. Late payment penalties add 5% to your unpaid tax after 30 days, with further penalties at 6 and 12 months [13].

Calculating Your Crypto Tax Liability

Understanding when do I pay tax on crypto UK requires knowing how to calculate what you owe. HMRC has specific rules for determining gains and losses.

Share Pooling and Same-Day Rules

Unlike shares, where you might track individual lots, HMRC requires you to pool fungible crypto assets of the same type. However, special ordering rules apply:

Same-day rule: If you buy and sell the same cryptocurrency on the same day, match those transactions first.

Bed and breakfasting rule: If you sell crypto and buy the same crypto within 30 days, match the sale with purchases in those following 30 days (in chronological order).

Section 104 pool: After applying the above rules, all remaining tokens of the same type go into a pooled cost basis. You track the total cost and total quantity, calculating an average cost per token [14].

This pooling method means you can't cherry-pick which tokens you're selling to minimise tax (unlike in some other jurisdictions). You're always selling from the pool at the average cost.

Calculating Gains and Losses

The basic formula is:

Disposal proceeds - Allowable costs = Gain or Loss

Disposal proceeds: The pound sterling value you received (or market value if you didn't receive cash).

Allowable costs: Your original purchase price plus transaction fees, plus any costs directly related to the disposal (like exchange fees).

Example: You bought 1 Bitcoin for £20,000 (including £100 fees). You later sold it for £35,000 (paying £150 in fees). Your gain is £35,000 - £20,000 - £150 = £14,850.

After calculating all your gains and losses for the tax year, you can deduct your annual Capital Gains Tax allowance (£3,000 for 2026/27). You pay tax only on gains above this threshold.

Losses and Carry-Forward

If you dispose of crypto at a loss, you can use that loss to offset gains in the same tax year. If your losses exceed your gains, you can carry the unused losses forward to future tax years indefinitely [15].

You must report losses to HMRC within four years of the end of the tax year in which they occurred, even if you have no gains to offset. This preserves your ability to use them in future.

This is a critical planning point: realising losses strategically can significantly reduce your overall tax burden over time.

Record-Keeping Requirements

HMRC expects you to maintain detailed records of all crypto transactions, including:

- Type of token

- Date of transaction

- Quantity

- Value in pounds sterling at the time

- Transaction fees

- Wallet addresses involved

- Purpose of the transaction

You must keep these records for at least five years after the 31 January filing deadline for the relevant tax year. For the 2026/27 tax year, that means keeping records until at least 31 January 2033 [16].

Given the complexity of tracking hundreds or thousands of transactions across multiple exchanges and wallets, professional crypto tax software or qualified advisors become essential for anyone actively trading.

How HMRC Tracks Crypto Transactions

A common misconception is that crypto's pseudonymous nature provides tax privacy. It doesn't. HMRC has extensive capabilities to track crypto transactions and identify non-compliant taxpayers.

Exchange Data Sharing

UK-based crypto exchanges are required to collect customer information under Know Your Customer (KYC) regulations. Many exchanges proactively share data with HMRC or respond to information requests.

Additionally, HMRC has data-sharing agreements with tax authorities in other jurisdictions. The OECD's Common Reporting Standard and the Crypto-Asset Reporting Framework (CARF), which the UK has committed to implementing, will create automatic exchange of crypto transaction data between countries [17].

Blockchain Analysis

HMRC uses blockchain analytics tools to trace transactions. While individual wallets may be pseudonymous, once HMRC links a wallet address to your identity (through exchange KYC, for example), they can trace all transactions involving that address.

The transparency of public blockchains means every transaction is permanently recorded and analysable. This is the opposite of privacy,it's a permanent, public ledger.

Nudge Letters and Investigations

HMRC has sent thousands of "nudge letters" to individuals it believes may have undeclared crypto gains. These letters aren't accusations but warnings that HMRC has information suggesting you may have tax obligations [18].

Receiving a nudge letter should prompt immediate action: review your crypto transactions, calculate any tax owed, and either confirm you're compliant or make a disclosure.

HMRC has also opened formal investigations into crypto tax evasion. Penalties for deliberate non-compliance can reach 100% of the tax owed, plus the original tax, plus interest.

The Digital Disclosure Service

If you've failed to report crypto gains in previous years, HMRC's Digital Disclosure Service allows you to voluntarily disclose and pay what you owe. Voluntary disclosure typically results in lower penalties than HMRC discovering the non-compliance themselves [19].

This isn't about promoting fear,it's about professional accountability. The evidence is clear: HMRC has the tools, the data, and the commitment to enforce crypto tax compliance.

Special Situations and Edge Cases

Crypto taxation involves numerous special situations that require careful consideration.

Crypto Received as Employment Income

If your employer pays you in cryptocurrency, this is employment income subject to Income Tax and National Insurance. Your employer should handle PAYE, but if they don't, you're still responsible for the tax.

The taxable amount is the pound sterling value of the crypto when you receive it. When you later sell that crypto, you'll have a Capital Gains Tax event, with your cost basis being the value you were taxed on as income.

Crypto Gambling and Gaming

Gambling winnings in the UK are generally tax-free, but HMRC may view crypto "gambling" on DeFi protocols or prediction markets as trading rather than gambling, particularly if you're doing it regularly or systematically.

Crypto earned through play-to-earn games is likely taxable income when received, with subsequent disposal creating Capital Gains Tax events.

Inheritance and Gifts

When you die, your crypto holdings form part of your estate for Inheritance Tax purposes. Your executors need access to your wallets and accurate valuations as of the date of death.

Gifts of crypto during your lifetime may be exempt from Inheritance Tax if you survive seven years after making the gift, but they're still potential Capital Gains Tax events (except gifts to spouses).

Crypto Held in Companies

If you hold crypto through a limited company, different tax rules apply. Companies pay Corporation Tax on crypto gains (currently 25% for profits above £250,000), not Capital Gains Tax.

There may be strategic reasons to hold crypto in a company structure, but this requires professional tax planning and comes with additional compliance obligations.

Practical Steps for Compliance

Understanding when do I pay tax on crypto UK is only valuable if you act on it. Here are practical steps for ensuring compliance.

1. Track Everything From Day One

Start maintaining detailed records immediately. Don't wait until tax season. Use crypto tax software (like Koinly, CoinTracker, or Recap) that integrates with exchanges and wallets to automatically track transactions.

At minimum, record every purchase, sale, trade, transfer, and receipt of crypto with dates, amounts, values, and fees.

2. Calculate Your Tax Position Regularly

Don't wait until January to discover you owe £50,000 in tax. Review your tax position quarterly or after major transactions. This allows you to:

- Set aside funds to pay your tax bill

- Make strategic decisions about timing future disposals

- Realise losses to offset gains if beneficial

3. Understand Your Annual Allowance

The £3,000 Capital Gains Tax allowance (for 2026/27) is valuable. If you're approaching the end of the tax year with gains below this threshold, you might strategically realise more gains tax-free. Conversely, if you're well above it, you might defer disposals to the next tax year.

4. Consider Professional Advice

Crypto taxation is genuinely complex, particularly if you're involved in DeFi, have transactions across multiple chains, or have both income and capital gains. The cost of professional advice from a qualified crypto advisor often pays for itself through legitimate tax savings and risk reduction.

At TrustCrypto Institute, we maintain a directory of Certified Crypto Advisors (TCCA) who have demonstrated competence in UK crypto taxation through rigorous assessment. This isn't about promoting our certification,it's about emphasising that professional standards matter when your financial and legal compliance is at stake.

5. File and Pay on Time

Set reminders well before the 31 January deadline. Aim to file by early January at the latest, giving yourself time to resolve any issues.

If you can't pay your full tax bill by the deadline, contact HMRC immediately to arrange a payment plan. They're generally willing to work with taxpayers who proactively communicate difficulties.

6. Keep Records Securely

Your transaction records, wallet addresses, and tax calculations should be backed up securely. If HMRC investigates, you'll need to produce detailed evidence of your calculations.

Consider both digital backups (encrypted cloud storage) and physical backups of critical information like wallet recovery phrases (stored securely offline).

Common Mistakes to Avoid

Even well-intentioned crypto holders make costly errors. Here are the most common mistakes we see:

Mistake 1: Thinking Crypto-to-Crypto Trades Aren't Taxable

This is perhaps the most widespread misconception. Every crypto-to-crypto trade is a disposal of the original asset, triggering a potential Capital Gains Tax event. You can't avoid tax by staying "in crypto" without cashing out to pounds.

Mistake 2: Not Reporting Because Gains Are Below the Allowance

If your total taxable income and gains require you to file Self Assessment for other reasons, you must report all crypto disposals, even if the gains are below the £3,000 allowance. HMRC wants to see the full picture.

Mistake 3: Losing Track of Cost Basis

If you can't prove what you paid for crypto, HMRC may assume a cost basis of zero, meaning your entire disposal proceeds become taxable gains. This is catastrophic for long-term holders who've lost early transaction records.

Mistake 4: Ignoring Small Transactions

Every transaction counts, no matter how small. That £50 worth of Bitcoin you used to buy coffee? Taxable disposal. Those tiny DeFi transactions? Each one potentially taxable. Small transactions add up to significant tax bills.

Mistake 5: Not Reporting Income from Staking or Mining

Many people correctly report sales but forget that staking rewards, mining income, and airdrops are separate taxable events, usually as income rather than capital gains.

Mistake 6: Assuming Losses Don't Need Reporting

If you want to carry losses forward to offset future gains, you must report them to HMRC within four years. Failing to report losses when they occur can mean losing the ability to use them later.

The Future of Crypto Taxation in the UK

While this guide focuses on current rules for 2026, the regulatory landscape continues to evolve.

Potential Regulatory Changes

HMRC regularly updates its Cryptoassets Manual as new situations arise. The implementation of the OECD's Crypto-Asset Reporting Framework will significantly increase automatic data sharing between tax authorities globally, making non-compliance increasingly difficult [20].

There's ongoing discussion about whether the current tax treatment is optimal. Some advocate for clearer de minimis exemptions for small transactions, while others push for treating crypto more like currency for tax purposes. As of 2026, however, no major structural changes have been implemented.

The Importance of Professional Standards

As crypto taxation becomes more complex and enforcement more rigorous, the need for qualified professionals grows. This is precisely why TrustCrypto Institute developed our assessment-led certification programmes for crypto advisors.

The baseline for crypto knowledge and professional conduct needs to rise. Investors deserve advisors who understand not just blockchain technology but UK tax law, FCA regulations, and professional ethics. Advisors need clear frameworks and rigorous assessment to demonstrate competence.

We're not promoting our certifications here,we're highlighting a genuine market need. The crypto advisory space has too many self-proclaimed "experts" with insufficient knowledge of UK regulatory requirements. Professional standards, transparent credentials, and verified competence matter enormously when your tax compliance is at stake.

Staying Current

Tax rules change. HMRC guidance evolves. Court cases create new precedents. If you hold significant crypto assets or advise others on crypto taxation, staying current isn't optional,it's essential.

Subscribe to HMRC updates, follow reputable UK crypto tax specialists, and consider ongoing professional development. For certified professionals, continuing professional development (CPD) requirements ensure knowledge stays current as the landscape shifts.

Conclusion: When Do I Pay Tax on Crypto UK? Your Action Plan

Let's bring this back to the fundamental question: when do I pay tax on crypto UK?

You pay tax when you dispose of cryptocurrency,selling it, trading it, spending it, or gifting it,or when you receive crypto as income through mining, staking, employment, or services. The tax is due by 31 January following the end of the tax year in which the taxable event occurred.

But knowing when isn't enough. Professional accountability demands action:

Immediate actions:

- Review all your crypto transactions from the current tax year (6 April 2026 to 5 April 2027)

- Identify which transactions are taxable disposals or income

- Begin tracking all future transactions systematically

- Calculate your approximate tax liability to date

Before 5 October 2027:

- Register for Self Assessment if you've never filed before and have taxable crypto events in 2026/27

Before 31 January 2028:

- Complete your 2026/27 Self Assessment return

- Pay any Capital Gains Tax or Income Tax owed

- Report any losses you want to carry forward

Ongoing:

- Maintain detailed records of all crypto transactions

- Review your tax position quarterly

- Consider professional advice if your situation is complex

- Stay informed about HMRC guidance updates

The evidence is clear: HMRC has the capability and commitment to enforce crypto tax compliance. The framework is established. The deadlines are non-negotiable. The penalties for non-compliance are significant.

But compliance isn't just about avoiding penalties,it's about professional integrity and long-term financial planning. Understanding your tax obligations allows you to make informed decisions, optimise your tax position legally, and build your crypto holdings on a solid foundation.

If you're a professional advisor, your clients depend on you to understand these rules thoroughly. If you're an investor, your financial future depends on getting this right. Either way, the standards matter.

At TrustCrypto Institute, we believe in raising the baseline for crypto knowledge and professional conduct. We've provided this comprehensive guide as part of our educational mission,not to sell you services, but to ensure you have the evidence-based information needed to make sound decisions.

Crypto taxation isn't going away. It's becoming more sophisticated, more enforced, and more integrated into the broader UK tax system. The question isn't whether to comply,it's how to do so efficiently and correctly.

Start today. Track your transactions. Understand your obligations. Seek qualified advice when needed. File and pay on time.

Your future self will thank you.

Related Resources

Explore these helpful tools and guides:

Take the Next Step

Ready to advance your crypto expertise? Explore our TCCS certification to enhance your professional credentials.

References

- [1] HMRC. HMRC (2024). "Cryptoassets Manual: CRYPTO10000 - Introduction: What are cryptoassets?" Gov.uk. https://www.gov.uk/hmrc-internal-manuals/cryptoassets-manual/crypto10000

- [2] HMRC. HMRC (2024). "Cryptoassets Manual: CRYPTO20000 - Types of cryptoassets." Gov.uk. https://www.gov.uk/hmrc-internal-manuals/cryptoassets-manual/crypto20000

- [3] UK Parliament. UK Parliament (1992). "Taxation of Chargeable Gains Act 1992." legislation.gov.uk. https://www.legislation.gov.uk/ukpga/1992/12/contents

- [4] HMRC. HMRC (2024). "Cryptoassets Manual: CRYPTO21200 - Exchange tokens: Capital Gains Tax: Disposing of exchange tokens." Gov.uk. https://www.gov.uk/hmrc-internal-manuals/cryptoassets-manual/crypto21200

- [5] HMRC. HMRC (2024). "Tax on cryptoassets: Giving cryptoassets to charity." Gov.uk. https://www.gov.uk/government/publications/tax-on-cryptoassets/cryptoassets-for-individuals#giving-cryptoassets-to-charity

- [6] HM Revenue & Customs. HM Revenue & Customs (2026). "Capital Gains Tax rates and allowances." Gov.uk. https://www.gov.uk/capital-gains-tax/rates

- [7] HM Revenue & Customs. HM Revenue & Customs (2026). "Income Tax rates and Personal Allowances." Gov.uk. https://www.gov.uk/income-tax-rates

- [8] HMRC. HMRC (2024). "Cryptoassets Manual: CRYPTO21000 - Exchange tokens: Is the individual trading?" Gov.uk. https://www.gov.uk/hmrc-internal-manuals/cryptoassets-manual/crypto21000

- [9] HMRC. HMRC (2024). "Cryptoassets Manual: CRYPTO40000 - Income Tax: Mining and transaction confirmation." Gov.uk. https://www.gov.uk/hmrc-internal-manuals/cryptoassets-manual/crypto40000

- [10] HMRC. HMRC (2024). "Cryptoassets Manual: CRYPTO61000 - Income Tax: Staking and other activities." Gov.uk. https://www.gov.uk/hmrc-internal-manuals/cryptoassets-manual/crypto61000

- [11] HMRC. HMRC (2024). "Cryptoassets Manual: CRYPTO21250 - Exchange tokens: Capital Gains Tax: Airdrops." Gov.uk. https://www.gov.uk/hmrc-internal-manuals/cryptoassets-manual/crypto21250

- [12] HMRC. HMRC (2026). "Understand your Self Assessment tax bill: Payments on account." Gov.uk. https://www.gov.uk/understand-self-assessment-bill/payments-on-account

- [13] HMRC. HMRC (2026). "Estimate your penalty for Self Assessment tax returns." Gov.uk. https://www.gov.uk/estimate-self-assessment-penalty

- [14] HMRC. HMRC (2024). "Cryptoassets Manual: CRYPTO21300 - Exchange tokens: Capital Gains Tax: Share pooling." Gov.uk. https://www.gov.uk/hmrc-internal-manuals/cryptoassets-manual/crypto21300

- [15] HMRC. HMRC (2026). "Capital Gains Tax: Report and pay Capital Gains Tax." Gov.uk. https://www.gov.uk/capital-gains-tax/report-and-pay-capital-gains-tax

- [16] HMRC. HMRC (2024). "Cryptoassets Manual: CRYPTO10200 - Introduction: Record keeping." Gov.uk. https://www.gov.uk/hmrc-internal-manuals/cryptoassets-manual/crypto10200

- [17] OECD. OECD (2023). "Crypto-Asset Reporting Framework and Amendments to the Common Reporting Standard." OECD Publishing, Paris. https://www.oecd.org/tax/exchange-of-tax-information/crypto-asset-reporting-framework-and-amendments-to-the-common-reporting-standard.htm

- [18] HM Revenue & Customs. HM Revenue & Customs (2024). "HMRC issues thousands of letters to cryptoasset investors." Gov.uk Press Release. https://www.gov.uk/government/news/hmrc-issues-thousands-of-letters-to-cryptoasset-investors

- [19] HMRC. HMRC (2026). "Tell HMRC about underpaid tax from previous years: Digital Disclosure Service." Gov.uk. https://www.gov.uk/tell-hmrc-about-underpaid-tax-from-previous-years

- [20] HM Treasury. HM Treasury (2024). "UK commits to implementing OECD Crypto-Asset Reporting Framework." Gov.uk. https://www.gov.uk/government/publications/implementation-of-the-oecd-crypto-asset-reporting-framework